Click image to enlarge

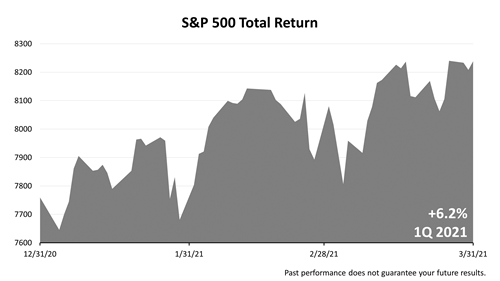

Stocks posted a +6.2% gain in the first quarter of 2021, following +12.2% gain in the fourth quarter of 2020. How many people here today think that a +6.2% quarter is a great quarter? How many of you think it is average? And how many think it is not so good? It’s always interesting to see how people perceive things. Now let’s see the returns on stocks for the past 25 quarters, instead of just a single quarter.

Click image to enlarge

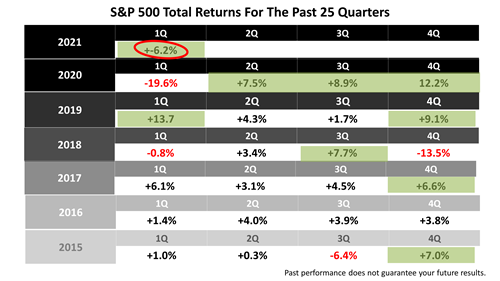

This table shows the last 25 quarters—six years and three months of quarterly results. The green-highlighted boxes indicate all the times in the past 25 quarters that the return on stocks was +6.2% or more. In nine of the last 25 quarters, the stocks returned +6.2% or more. So let me ask you again: How many people here today think that a +6.2% quarter is a great quarter? How many of you think it is average? And how many think it is not so good? Okay, so what’s the answer? The answer is that a +6.2% return in three months is amazing! And the last 25 quarters have been amazing, as well! What is even more amazing is that the outlook for the U.S. economy and U.S. stocks is very bright.

Click image to enlarge

The role played by the government in responding to the COVID economic crisis will be subject to political debate. Whether you are for or against the stimulus and government aid in response to the COVID pandemic does not matter to the stock market. No matter the politics, all that matters is the numbers, and the numbers unmistakably indicate an unprecedented boom is underway.

Click image to enlarge

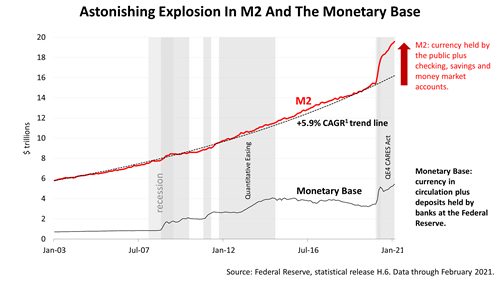

Now, this is absolutely astounding. Look at the surge in the money supply. Never seen anything like it, at least in my career! And I don't think there is anything like it in the economic history. The surge in M2 is a really big deal. What is M2? M2 is cash, checking, savings, and money market accounts. It's money that's in the hands of people and ready to be spent. It's available to spend. It’s very different from the stimulus the Federal Reserve applied in a series of major monetary actions that brought the economy back from brink of disaster in the world financial crisis of 2008. Quantitative easing programs by the Fed to pump liquidity into the banking system are ongoing and a powerful new tool in the Fed’s arsenal, but QE only expands the monetary base; it doesn’t put money in people’s pockets. This explosion in M2 has been fueled by the 37 million economic stimulus checks the IRS said this week that it was sending out, upping the total number distributed to Americans to 127 million. That money has got to go somewhere! It absolutely will be spent on home improvements, leisure activities, lawnmowers, nightclubs, and the usual ways Americans always find to consume more stuff. That will boost corporate earnings, and earnings drive stock prices. But some of that stimulus money can reasonably be expected to find its way into stocks, bonds, and real estate—also known as risk assets because they carry some risk but pay capital gains. House prices are up 10% from a year ago. With record-low interest rates and record cash in people’s accounts, it’s no wonder prices on capital-appreciation assets are finding new record highs. The M2 statistic is absolutely astounding.

Click image to enlarge

To recap the current financial economic situation, the stock market has been on a roll, providing fantastic returns for years, and the explosion in M2 is signaling the beginning of unprecedented growth in 2021 and 2022, which could fuel higher stock prices in the months ahead.

Click image to enlarge

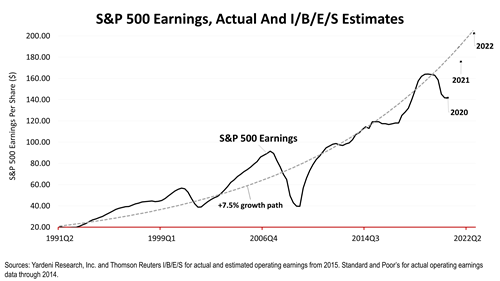

The stock market for months has been very definitely reacting to, first and foremost, the recovery in earnings estimates to pre-pandemic levels. Earnings drive stock prices. So, let’s look at current earnings growth and the outlook, as of April 1, 2021, through the end of 2022.

Click image to enlarge

In 2020, actual earnings of the S&P 500 were $141.51. Expected earnings in 2021, according to Wall Street analysts’ estimates compiled by Institutional Brokers' Estimate System (IBES), are $175.55 and expected to shoot up to $202.30. The red arrows drawn in here literally connect the dots to make the forecast clear: The next 20 months’ corporate earnings are expected to rocket almost straight up. The gray dotted line shows the +7.5% long-term earnings growth trend since 1991. To be clear, the outlook based on Wall Street’s earnings forecast is that, at the end of 2022, corporate earnings growth will recover fully from the pandemic; it will be as if the pandemic never happened. And 2021 and 2022 S&P 500 earnings estimates have continued to be revised higher for months. To be clear, the 2022 earnings growth number is now back to the long-term trend rate of growth. Earnings are fully recovered from the COVID stock-market wipeout, when the market bottomed after losing -33.9% of its value. I want to say that again—a -33.9% drop in market value occurred just a little over a year ago. 2020 (actual), 2021 (estimated), and 2022 (estimated) bottom-up S&P 500 operating earnings per share as of April 1, 2021: for 2020(a), $141.51; for 2021(e), $175.55; for 2022(e), $202.30. Sources: Yardeni Research, Inc. and Thomson Reuters I/B/E/S for actual and estimated operating earnings from 2015. Standard and Poor’s for actual operating earnings data through 2014.

Click image to enlarge

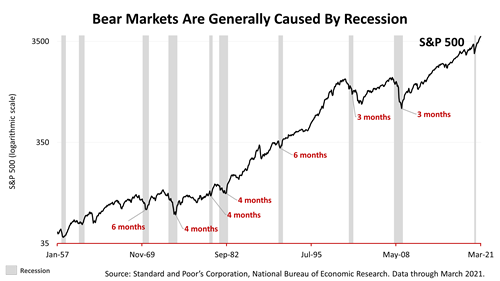

Keep in mind, it generally takes a recession to cause a bear market in stocks. This chart spans modern American financial economic history, and in the gray bands are the recessions. The big downturns in the stock market almost all occurred concurrent with recessions…

And that's not where we're headed right now. We're not headed for another recession right now. We just had a recession! In fact, because of the surge in M2, we’re in an unprecedented boom!

Click image to enlarge

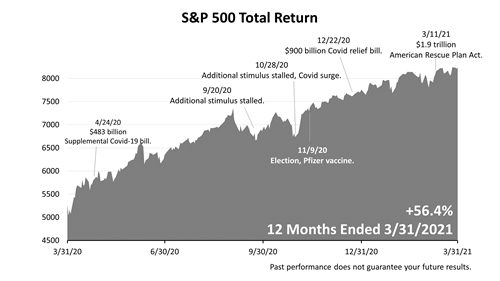

Here’s a visualization of the stock market’s performance from the last five years. This gives you a much better view into what an unusual period the last few years has been. Two bear markets—in December 2018 and February 2020—in the last two and one-half years! After trading sideways for approximately two years in 2015 and most of 2016, hitting two air pockets during that period, the stock market broke out after the November 2016 election and rose steadily to an all-time peak on September 20, 2018, whereupon it dove by -20% on investor fears that an inverted yield curve was imminent. On January 4, 2019, the Fed signaled rates were on hold, whereupon stocks rallied for most of the remainder of 2019. In February of 2020, stocks hit a new all-time peak; then the COVID-19 virus put the economy and the stock market into meltdown. By early September of 2020, stocks hit a record all-time high following the enactment of CARES and related legislation. After a pause, stocks rallied steadily from the November 2020 election through year-end. Stocks continued upward through the first quarter of 2021 with the March enactment of the $1.9 trillion American Rescue Plan Act. And the third round of stimulus checks will hit accounts in April and May. Over the last five years, including dividends, the S&P 500 Total Return index has gained +113%. As the second quarter gets under way, a market melt-up is possible. Here’s why.

Click image to enlarge

What’s The Risk Of A Market Melt-Up?

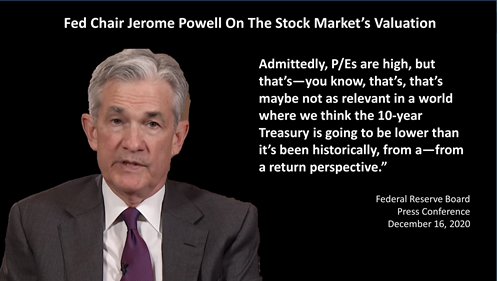

The Standard & Poor’s 500 stock index closed today at 4164.66, 1% off its all-time high of 4211.47 set last Thursday. Stocks have continued to break records for months and a market melt-up is possible. Are stocks fairly priced? For the answer, we turn to Jerome Powell, the U.S. Federal Reserve Bank chairman. Fed chairmen generally avoid talking the stock market up or down. However, at a recent press conference, Mr. Powell was asked about the fact that stocks are highly priced by traditional valuation standards like price-to-earnings (P/E) ratios. Mr. Powell’s answer is important to investors, though it did not get much press. That day, the East Coast faced the worst winter storm in years and a lot of things were going on, as always. But here’s what Mr. Powell said: “Admittedly, P/Es are high, but maybe that's not as relevant in a world where we think the 10-year Treasury is going to be lower than it's been historically.” The Fed chair is saying stocks are not overpriced compared to bond yields, which are going to be low for a sustained period. The Fed is saying pay no attention to the market's P/E ratio; it’s more relevant in the current conditions to value the market's P/E ratio relative to bond yields. On that basis, stocks aren't expensive. Mr. Powell is saying the P/E ratio isn't so relevant right now because of the low-interest-rate situation worldwide. He’s saying that what's most important is the comparison of the P/E ratio to bond yields. Fascinating. It's important because, to the extent that the Fed chairman believes this, then he's going to remain accommodative and keep creating money, aiding and abetting the Treasury in creating money. That's going to continue to support stocks, as well as the economy, for the foreseeable future. At least, that's a conclusion that one could reasonably reach. In contrast to Alan Greenspan, who warned stock investors were growing irrationally exuberant in 1996, four years before the peak in a great bull market, this Fed chairman is saying: Pay no attention to P/E ratios, the traditional valuation benchmark of stocks. What matters is the P/E ratio compared to the 10-year bond yield, and that bond yields are likely to remain low for the foreseeable future because of population trends in developed and developing nations, improvements in technology, and other fundamentals. If the Fed thinks high price-to-earnings ratios are not relevant and bond yields relative to stock prices are a better measure in current economic conditions, then that leaves leeway for stocks to rise without Fed action. The risk of a market melt-up is a real thing. If you fear missing out on a market melt-up or are worried about being overexposed to stock risk, consider designing a core portfolio diversified across low-expense assets and professionally managed.

Click image to enlarge

Fed action to raise rates and slow the economy largely hinges on inflation. This is the inflation number to keep your eye on. You can look at inflation measured lots of different ways, but I think this is a good measure. This is the personal consumption expenditures deflator. The PCED is the inflation index quoted by the Fed to set policy, not the much better known Consumer Price Index, or CPI. The PCED index number has been trending higher at +1½%. The lower gray dotted line is a 1.5% long-term compound annual growth rate. The Fed has been saying for many years that the optimal long-term inflation rate is +2% annually, but the inflation rate for a decade has drifted along a +1.5% annualized inflation rate—far below the Fed’s target. So, what the Fed has been saying, and what they are likely to continue to say, is that, “Until this curve bends towards a 2% slope, we're not going to consider that our job is complete, and we are going to remain accommodative.” And you can see how persistent this index has been at +1½%. Based on the Fed chair’s public pronouncements, unless the slope of this curve bends to the +2% slope in the gray dotted trend line, the Fed will not change course or deem that they have accomplished their inflation goal of +2%. The Fed has said it will not act until a sustained period of 2%-plus inflation.

Click image to enlarge

Here’s Ed Yardeni, one of the most respected economists in the country, last week, saying there is no sign of a wage-price spiral, at least not yet. Wages are the key to inflation. You’ve heard probably a lot about commodity prices. Commodity prices are not immaterial, but are much, much less important to the overall inflation picture than wages, because 60% of corporations’ costs are wages and benefits. So, it's really a wage-price spiral that you need to worry about. And unless and until we start to see that, I think the Fed will remain very relaxed over the inflation outlook.

Click image to enlarge

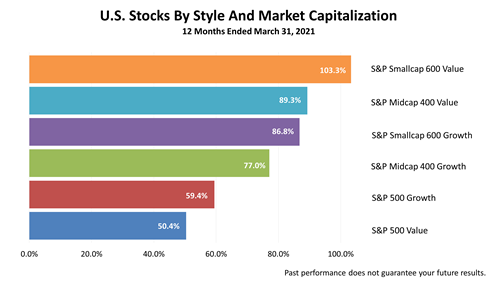

While a single quarter of data is usually not elucidating—it’s just not enough time and data to make a sweeping conclusion—sometimes a single quarter tips you off to a shift in investor preferences. That’s true in this three-month snapshot. This shows the stock market investments, classifying companies by market capitalization and style. Small-cap value and mid-cap value stocks were the best performers.

Click image to enlarge

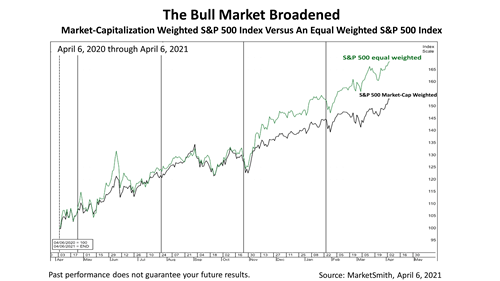

That marked a reversal from the pandemic boom in the super-cap growth stocks, like Amazon, Apple, Facebook, Microsoft, Netflix, and Google—the FAANGM—which dominated returns and temporarily distorted the performance of the S&P 500 index. Early in the COVID crisis, the FAANGM grew stronger because their solutions were used more than expected, triggering larger-than-expected profits in a handful of stocks. Since the S&P 500 index is market weighted, the price surge in the super-large tech companies became more influential in the S&P 500 index. That trend was reversed last quarter, and again in the first quarter of 2021 ended March 31. The role played by the government in responding to the COVID economic crisis will be subject to political debate. No matter what you think of the massive government aid, however, the broadening of the bull market is a very positive trend for stock market investors.

Click image to enlarge

In this chart, the equal-weighted Standard & Poor’s 500 stock index is outperforming the market-capitalization-weighted S&P 500 index, which is commonly quoted and the main benchmark of U.S. stock performance. Since the election, you can see here how the bull market broadened out. Value and small-cap stocks have surged.

Click image to enlarge

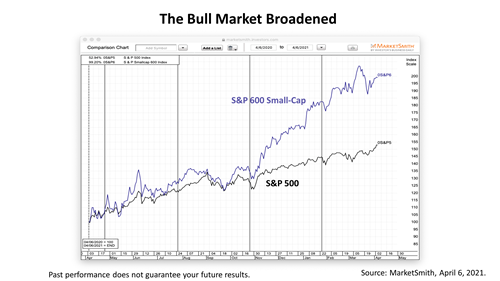

Here’s another snapshot of the broadening in the performance of the S&P 500: The S&P small-cap index is outperforming the market-cap-weighted S&P 500. They’re playing catch-up because the large-cap growth stocks had been so dominant and were driving the returns on the S&P 500 index.

Click image to enlarge

What’s more important than the broadening showing up in returns last quarter is this chart, showing the past 12 months.

Click image to enlarge

Click image to enlarge

The 12 months ended March 31, 2021, was a period like no other before. The stock market low after the pandemic struck was on March 23, 2020, a week before this chart starts. While not including the frightening -33.9% bear market plunge from early February through March 23rd, you can see the spectacular bull market eruption amid the crisis. The stock market is always looking ahead, and once the worst of the pandemic news was out, the series of stimulus packages helped fuel a bright outlook.

Click image to enlarge

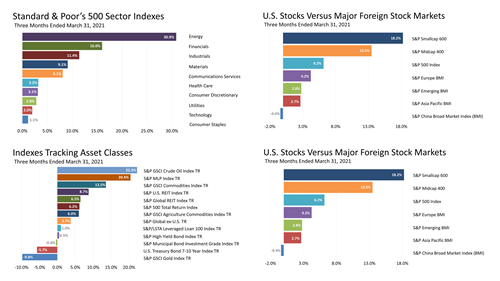

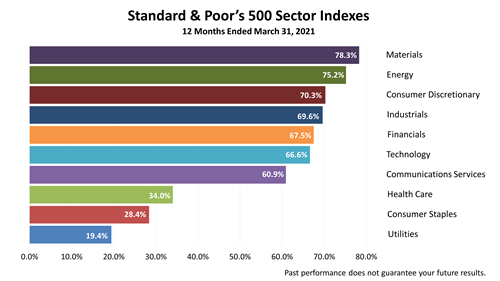

Not that predicting which sectors will outperform is possible, this bar graph shows which industry sectors in the S&P 500 had the best and worst returns in the 12 months through March 2021. Slow and steady definitely did not win the race, with utilities and consumer staples trailing the growth sectors sharply.

Click image to enlarge

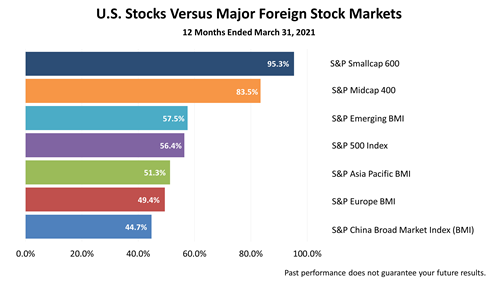

With so much focus on the rising power of the People’s Republic of China, it is interesting that the Chinese stock market sharply trailed the U.S. Even more interesting, China accounts for a large part of the Emerging Markets Index, and yet it sharply underperformed that index, as well as the U.S. stock market indexes. For all the concern about the rise of China, the Chinese stock market remains risky because it is largely government-controlled.

Click image to enlarge

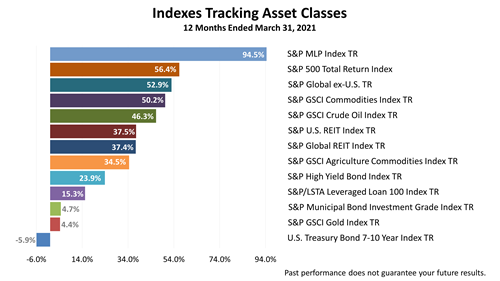

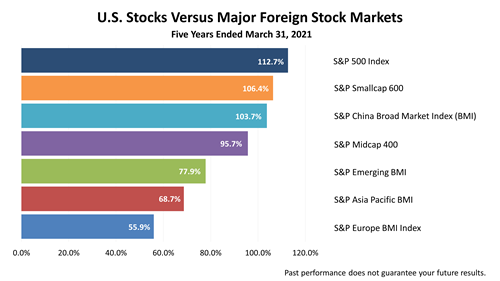

With a return to something closer to normalcy in sight, master limited partnerships (MLPs), which are heavily invested in energy-related companies, nearly doubled in value in the 12 months ended March 31, 2021. The other notable data point: The intermediate-term U.S. Treasury Bond Index lost -5.9%. Interest rates are low and are not likely to change much in the foreseeable future, making the bond outlook weak. Foreign markets provided little more than half the return on stocks in this 12-month period, continuing the long-term trend of U.S. returns outperforming the world’s equities markets.

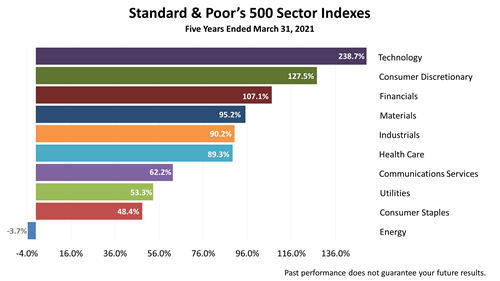

Click image to enlarge

Tech stocks more than tripled in the five years ended March 31, 2021, and, amazingly, despite the pandemic, discretionary consumer companies more than doubled.

Click image to enlarge

While we just reviewed a few minutes ago how energy stocks in the last 12 months were spectacular outperformers, look at the five-year figures in the chart on the top left. Over five years, energy stock investments, as represented by the Standard & Poor’s Energy Index, lost -3.7%. Which makes this a perfect time to remind you that data history is so important to investment analysis. You need to be able to consider current conditions with a clear understanding of history.

Click image to enlarge

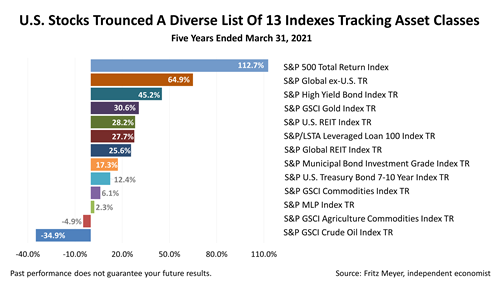

U.S. Stocks Returned 10 Times More Than Bonds In Past Five Years The U.S. stock market trounced returns on a diverse group of 13 indexes tracking major asset classes in the five years ended March 31, 2021. U.S. large-company stocks returned twice as much as foreign stocks and 10 times as much as intermediate-term bonds. U.S. stocks are the main growth engine of a prudently designed, broadly diversified portfolio, which makes the extraordinary outperformance by stocks fantastic news for U.S. retirement investors guided by modern portfolio theory and tracked in articles and newsletters published here. And with the economy about to boom, the stock market could keep breaking records, as it has done for months.

Click image to enlarge

Click image to enlarge

No one can predict the stock market’s performance. Taxes are more predictable and important at this moment in history. If maintaining a disciplined strategy based on facts, continual research, and best practices in the financial advice profession is important to you, please do not miss the tax-planning opportunities that are about to close. President Joseph Biden’s speech before a joint session of the U.S. Congress tonight spelled an end to a bevy of tax opportunities. For high-income earners and high-net-worth individuals, the tax train is leaving the proverbial station. If your income is going to be above $400,000, or if you or your parents own a couple of homes and a retirement portfolio, you could easily be affected by the changes that are widely expected. Act before the effective dates of higher capital gains, estate, and income taxes that are widely expected are enacted in the days ahead.

Click image to enlarge

|